Micro-loans: The new financial lifeline for South Africans

Context mode is active. Hover over any highlighted term to see its definition. Click a nested term to go deeper.

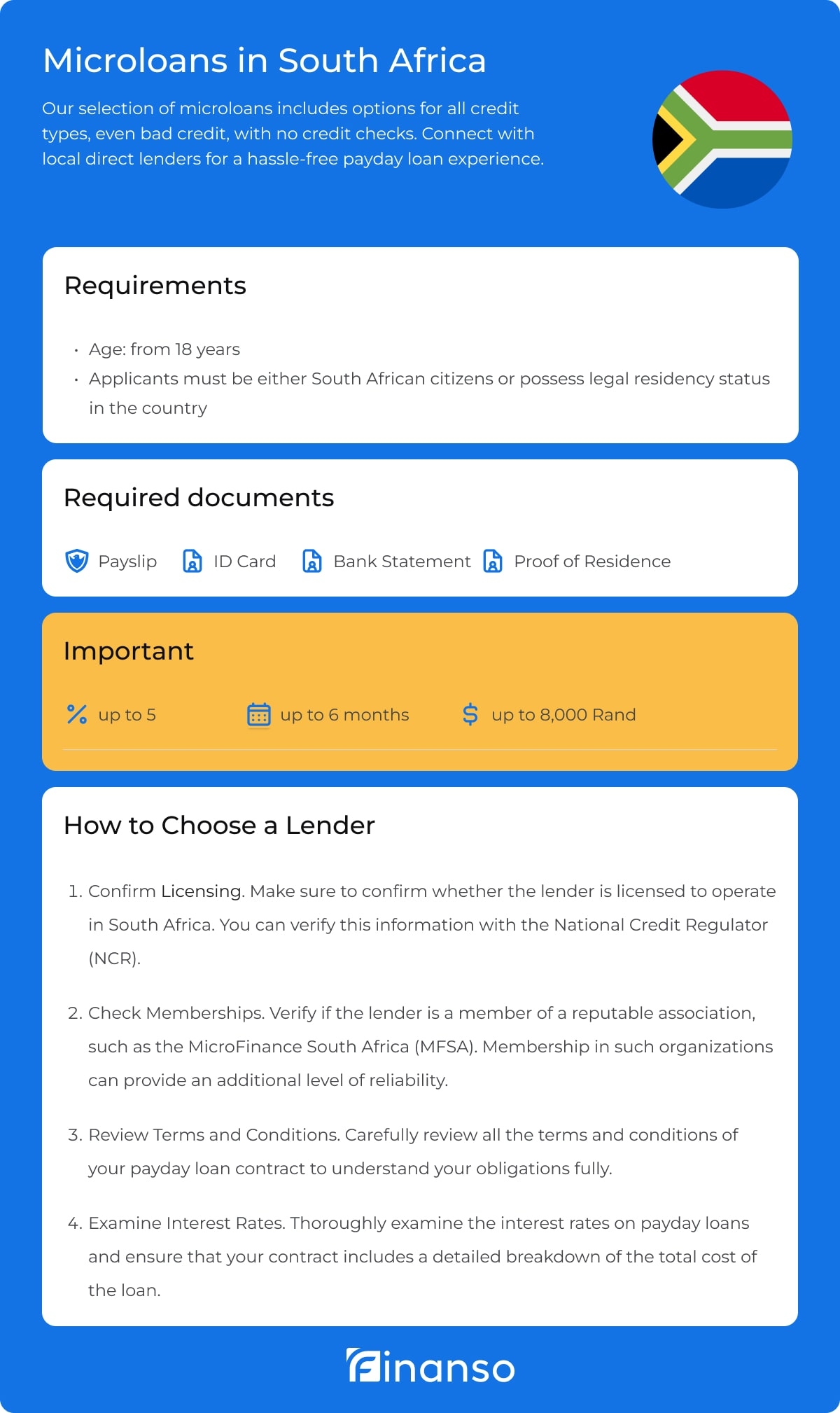

South Africa's consumer credit landscape is undergoing a silent but significant transformation. The latest Q1 2026 data from the National Credit Regulator (NCR) reveals a dramatic surge in the number of micro-loans, often below R5,000, even as the average size of traditional personal loans shrinks. This signals a troubling shift where millions of South Africans are increasingly relying on high-cost, short-term debt simply to cover daily survival expenses, rather than for asset acquisition. This trend underscores the deepening financial fragility exacerbated by persistent inflation, high unemployment, and the ongoing burden of load shedding. While the South African Reserve Bank (SARB) continues its hawkish stance to curb price increases, elevated interest rates are simultaneously making all forms of credit more expensive. Credit bureaus are reporting a corresponding rise in consumer credit impairment, pushing more households into a vicious cycle of over-indebtedness, with a growing segment turning to less regulated micro-lenders as a last resort. Regulators like the NCR and the Financial Sector Conduct Authority (FSCA) face mounting pressure to enhance oversight of the micro-lending sector, especially as innovative fintechs enter the market, blurring the lines of regulation. Policymakers must now grapple with balancing access to credit for the unbanked against the imperative of consumer protection. The trajectory of household debt and credit quality in the coming quarters will be a critical indicator of South Africa's broader economic health.